Could an undetected discrepancy in your benchmarking methodology under Federal Decree-Law No. 47 of 2022 inadvertently trigger a retroactive tax adjustment that threatens your organization’s financial integrity? Many sophisticated enterprises currently struggle with the technical nuances of “Connected Persons” definitions, as the transition to the 9% corporate tax rate necessitates a level of documentation that was previously non-compulsory in the local market. We recognize that the inherent complexity of identifying comparable uncontrolled transactions often generates significant uncertainty, yet it’s essential to establish a defensible position before the authorities. This comprehensive guide is designed to help you master the complexities of transfer pricing in uae, ensuring that every intercompany arrangement strictly adheres to the arm’s length principle and Federal Tax Authority mandates. By facilitating a deeper understanding of Master File and Local File requirements, we’ll demonstrate how to implement a robust governance framework that mitigates the risk of an audit while optimizing your tax structure within established legal boundaries.

Key Takeaways

- Understand the regulatory mandates of Federal Decree-Law No. 47 of 2022 to ensure your enterprise maintains full compliance with the Federal Tax Authority’s governance standards.

- Distinguish between Related Parties and Connected Persons to meticulously apply the arm’s length principle to all domestic and international intercompany transactions.

- Determine if your business meets the AED 200 million revenue threshold necessitating the preparation of statutory Master and Local Files for transfer pricing in uae.

- Identify the most appropriate benchmarking methodologies to align your fiscal reporting with International Financial Reporting Standards and withstand rigorous statutory audits.

- Explore how a strategic advisory partnership facilitates proactive risk assessments and transforms mandatory tax compliance into a strategic advantage for corporate growth.

The Regulatory Framework of Transfer Pricing in the UAE

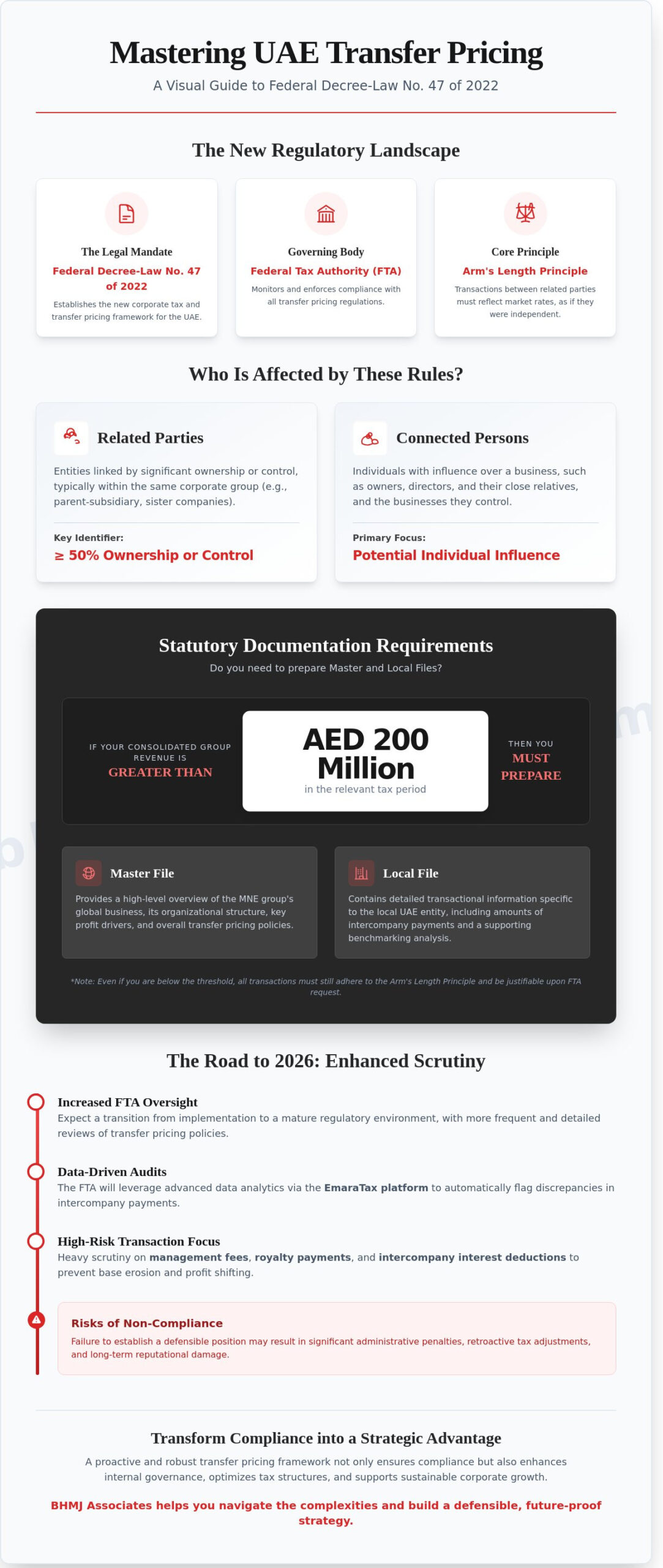

The introduction of Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses marks a transformative era for the United Arab Emirates. This legislative framework mandates that all taxable persons, whether they operate within the mainland or designated free zones, must ensure their intercompany dealings align with international standards. The Federal Tax Authority (FTA) now possesses the mandate to monitor both cross-border and domestic transactions with rigorous oversight, ensuring that every taxable person adheres to the statutory requirements designed to protect the integrity of the national tax base. To establish a baseline for these requirements, one should first clarify What is Transfer Pricing? within the context of global tax governance. It’s a fundamental concept that dictates how prices are set for transactions between related parties to prevent profit shifting and ensure fiscal transparency.

To better understand how these regulations impact your business operations, watch this professional overview:

The Legal Basis for Transfer Pricing

Article 34 of the Corporate Tax Law serves as the cornerstone of transfer pricing in uae, explicitly requiring that transactions between related parties and connected persons meet the Arm’s Length Principle. This principle ensures that financial results are consistent with those that would’ve been achieved between independent parties under similar circumstances. Ministerial Decision No. 97 of 2023 further clarifies the documentation requirements, necessitating the maintenance of Master Files and Local Files for entities exceeding specific revenue thresholds. The UAE’s framework doesn’t operate in isolation; it integrates the OECD Transfer Pricing Guidelines to facilitate a standardized approach to international fiscal compliance. Our firm views these regulations as a strategic mechanism for value addition, rather than a mere statutory hurdle.

The Significance of 2026 Compliance

The 2026 compliance cycle serves as the definitive transition from initial implementation to a period of mature regulatory oversight. We expect the FTA to utilize advanced data analytics to identify discrepancies in cross-border payments, focusing heavily on management fees, royalty payments, and intercompany interest deductions. The shift toward digital transparency through the EmaraTax platform requires that every fiduciary record is meticulously maintained to withstand the complexities of a formal audit. Businesses must view these requirements as a strategic opportunity to enhance their internal governance and ensure long-term sustainability. Failure to implement robust transfer pricing in uae structures today may lead to significant administrative penalties and reputational risks during the 2026 audit cycle. Our role is to facilitate this transition, ensuring your enterprise remains a stable and ethical participant in the UAE economy.

Defining Related Parties and the Arm’s Length Principle

Under the regulatory framework established by Federal Decree-Law No. 47 of 2022, which became effective on June 1, 2023, the identification of Related Parties is the cornerstone of transfer pricing in uae. This legislation mandates that all transactions between entities with shared ownership or control must be conducted with the same financial rigor as those between independent third parties. Taxable persons must differentiate between Related Parties, which typically encompass entities within the same corporate group, and Connected Persons, who include owners, directors, and their relatives. While the former focuses on institutional structures, the latter addresses the potential for individual influence over business expenditures and income distribution.

Identifying Related Parties and Control

The UAE Corporate Tax law establishes a clear 50% threshold for ownership interest to determine control, yet the definition of a Related Party extends far beyond simple shareholding percentages. Significant influence may be exerted through voting rights, the power to appoint board members, or through substantial debt financing that dictates operational decisions. Fiduciary relationships and kinship up to the fourth degree of affiliation are also scrutinized to prevent the erosion of the tax base. Our team works to facilitate a strategic advantage by mapping these complex relationships to ensure every intercompany interaction is documented with statutory precision.

The Arm’s Length Standard in Practice

The Arm’s Length Principle serves as the international benchmark for fair value in intercompany dealings. To adhere to this standard, businesses must evaluate their controlled transactions against uncontrolled market conditions involving independent parties. This process requires a thorough analysis of comparable circumstances, including the functions performed, assets employed, and risks assumed by each party. The OECD Transfer Pricing Guidelines provide the essential framework for this comparison, which the Federal Tax Authority (FTA) utilizes as a primary reference for audit purposes. When transfer pricing in uae doesn’t align with market realities, the resulting adjustments to taxable income lead to significant fiscal consequences, including the reassessment of tax liabilities and the imposition of administrative penalties.

- Functional Analysis: Documenting the specific roles each entity plays in a transaction to ensure accurate pricing.

- Risk Profiling: Identifying which party bears the financial and operational risks to justify profit allocation.

- Economic Comparability: Selecting market data that reflects the current UAE economic climate and specific industry benchmarks.

Ensuring compliance isn’t just about avoiding penalties; it’s about building a robust governance structure that supports long-term growth. By maintaining meticulous records that prove the arm’s length nature of transactions, firms can protect their reputations and ensure their fiscal stability in a rapidly evolving regulatory environment. This disciplined approach to financial oversight provides the security necessary for sustainable corporate development.

Statutory Documentation Requirements: Master Files and Local Files

The regulatory environment surrounding transfer pricing in uae necessitates a disciplined approach to documentation, ensuring that all intercompany arrangements reflect the arm’s length principle with absolute precision. Under the current corporate tax regime established by the Federal Tax Authority, Taxable Persons must adhere to a two-tiered documentation structure if they meet specific financial thresholds. This framework is designed to provide tax auditors with a transparent view of how a business operates both as an independent entity and as part of a larger corporate group. Compliance isn’t a retrospective exercise; the law requires that documentation is prepared contemporaneously with the filing of the tax return to ensure that the economic justifications for pricing decisions are captured at the time transactions occur.

The obligation to maintain these files is triggered when a Taxable Person’s consolidated group revenue reaches or exceeds AED 200 million in the relevant tax period. Even for those below this threshold, specific disclosure requirements apply if the value of controlled transactions with related parties or connected persons exceeds AED 40 million. Detailed guidance on these specific reporting thresholds and the necessary administrative forms is accessible through the UAE Transfer Pricing Guide, which serves as the definitive reference for maintaining statutory transparency. Failure to maintain these records can lead to significant administrative penalties and may result in the tax authority making its own adjustments to the taxable income of the business.

The Master File: A Global Perspective

The Master File serves as a high-level overview of the Multinational Enterprise (MNE) group’s global operations, providing the authorities with a comprehensive understanding of the group’s organizational structure and its primary drivers of business profit. This document must detail the group’s intangible assets, including research and development activities and licensing agreements, alongside its intercompany financial arrangements and consolidated financial statements. It’s essential that the global policies described in the Master File align seamlessly with the operational realities of the UAE entity. Discrepancies between global policy and local execution often signal a lack of governance that could trigger a formal inquiry during a tax audit.

The Local File: UAE Entity Specifics

While the Master File looks outward, the Local File focuses inward on the specific activities of the UAE taxpayer, providing a granular analysis of all material intercompany transactions. This document must be supported by a rigorous functional analysis that evaluates the functions performed, assets employed, and risks assumed (FAR) by the UAE entity to ensure that the economic substance of the business is accurately reflected. To validate the arm’s length nature of these transactions, companies must conduct economic benchmarking using data from independent companies operating in similar market conditions. This empirical evidence is vital for demonstrating that transfer pricing in uae adheres to international standards, effectively transforming a compliance burden into a strategic advantage for long-term fiscal stability.

Benchmarking and the Role of Statutory Audit

The implementation of Federal Decree-Law No. 47 of 2022 has elevated the necessity for rigorous benchmarking to ensure that transfer pricing in uae adheres to the arm’s length principle. Selecting the most reliable method is not merely a compliance exercise; it is a strategic requirement that necessitates a deep functional analysis of the entities involved. Taxpayers must evaluate the Comparable Uncontrolled Price (CUP) method, the Resale Price Method, the Cost Plus Method, the Transactional Net Margin Method (TNMM), and the Profit Split Method to determine which provides the most accurate reflection of market conditions. While the CUP method is often preferred for its directness in commodity transactions, the TNMM has become a prevalent choice for service-oriented entities in Dubai and Abu Dhabi due to the availability of comparable financial data in regional benchmarking databases.

Transfer Pricing Methods and Selection

The selection process requires a methodical evaluation of the strengths and weaknesses of each recognized method in relation to the specific transaction type. Professionals utilize sophisticated benchmarking databases to extract financial data from independent companies that mirror the functional profile of the tested party. It’s essential that firms document the rationale for rejecting specific methods; failure to provide a logical justification for bypassing the CUP or Resale Price methods can lead to immediate scrutiny from Federal Tax Authority (FTA) inspectors. Accuracy in these selections facilitates a stable tax environment and protects the entity from retrospective adjustments that could impact liquidity.

Audit Assurance and Regulatory Alignment

The intersection of International Financial Reporting Standards (IFRS) and tax compliance is most visible during the statutory audit process, where auditors must ensure that related-party transactions are disclosed in accordance with IAS 24. A statutory audit provides the first line of defense in validating transfer pricing compliance. Auditors are tasked with verifying that the financial statements accurately reflect the economic reality of intra-group arrangements, ensuring that no artificial profit shifting has occurred to erode the UAE tax base. This oversight ensures that the fiduciary responsibilities of the board are met while maintaining alignment with global transparency standards.

Regulatory inquiries are often triggered by specific “Red Flags” identified during the audit or tax filing process. These include persistent operating losses in a local subsidiary while the global group remains profitable, or significant year-end adjustments that alter the taxable base by more than 10 percent. Additionally, management fees or royalty payments that lack a clear benefit test or supporting economic substance are frequently challenged. By maintaining a robust Transfer Pricing Local File, businesses can proactively address these concerns before they escalate into formal disputes or audit qualifications.

To ensure your organization maintains the highest standards of governance and mitigates regulatory risk, you should partner with our expert advisory team for a comprehensive review of your statutory audit and benchmarking protocols.

Navigating Compliance with BHMJ Associates: A Strategic Partnership

BHMJ Associates operates at the intersection of technical tax proficiency and rigorous audit standards. This dual approach ensures every fiscal strategy aligns with Federal Decree-Law No. 47 of 2022. We facilitate the entire corporate tax registration process. Our team ensures enterprises meet statutory obligations without delay. We conduct exhaustive risk assessments to identify vulnerabilities in intercompany transactions. Strategic advisory on business restructuring is a core pillar of our service. We help enhance compliance efficiency while maintaining operational fluidity. This meticulous fiduciary oversight secures long-term sustainability for our partners. It’s about more than simple filing; it’s about building a resilient corporate structure.

Our methodology focuses on the integration of global best practices with local regulatory nuances. We don’t just provide templates. We develop bespoke frameworks that reflect the economic reality of your operations. By blending audit-level scrutiny with tax advisory, we provide a level of assurance that standalone tax firms often miss. This comprehensive oversight is essential for managing the complexities of transfer pricing in uae, where the regulatory environment continues to evolve rapidly.

Comprehensive Tax Advisory Services

Our advisory extends to the intricate relationship between VAT and transfer pricing protocols. Adjustments in intercompany pricing often necessitate revisions to VAT returns previously filed at the 5% rate. We manage these corrections to prevent discrepancies that might trigger audits. We prepare robust Master and Local files that strictly adhere to Ministerial Decision No. 97 of 2023. These documents provide the necessary evidence of arm’s length transactions. If disputes arise, BHMJ Associates provides expert representation before the Federal Tax Authority. We ensure your technical positions are defended with professional rigour and documented evidence. Our goal is to resolve complex tax matters through clear, evidence-based communication with regulators.

Value Addition Through Professional Rigour

We enhance shareholder value by establishing regulatory certainty and mitigating the risk of administrative penalties. Cabinet Decision No. 75 of 2023 outlines significant fines for non-compliance. Our proactive governance eliminates these fiscal threats. A dedicated partner managing both statutory audit and tax compliance creates a cohesive financial ecosystem. This integration allows for a more granular understanding of your business’s value drivers. It’s a strategic advantage. We move methodically through your financial data to ensure every transaction is defensible. Your enterprise can initiate a comprehensive health check for transfer pricing in uae today. This process identifies gaps before they become liabilities. Contact our team to begin a diagnostic review of your current documentation and intercompany agreements.

Fortifying Corporate Governance in a Shifting Regulatory Landscape

The evolution of the United Arab Emirates’ fiscal environment, anchored by Federal Decree-Law No. 47 of 2022, necessitates a disciplined approach to corporate oversight. Mastering the complexities of transfer pricing in uae requires more than just meeting the basic arm’s length principle; it demands the meticulous preparation of Master and Local Files that align with international IFRS standards. Organizations must prioritize rigorous benchmarking and statutory audit processes to ensure intercompany transactions remain defensible under scrutiny from the Federal Tax Authority. If you don’t establish these frameworks early, the risk to your firm’s fiduciary standing increases significantly.

BHMJ Associates provides the authoritative guidance needed to navigate these regulatory shifts. Our firm utilizes advanced compliance management platforms like Odoo and Zoho to facilitate seamless reporting and data integrity. By integrating deep expertise in UAE Corporate Tax Law with a commitment to value addition, we transform statutory obligations into strategic advantages. It’s our mission to protect your enterprise through precise financial oversight and professional assurance. Consult with our expert partners for a comprehensive Transfer Pricing Risk Assessment. We’re dedicated to helping your business thrive within this new era of transparency and growth.

Frequently Asked Questions

Is transfer pricing only applicable to cross-border transactions in the UAE?

Transfer pricing in the UAE isn’t restricted to international dealings; it encompasses domestic transactions between related parties and connected persons as mandated by Federal Decree-Law No. 47 of 2022. The Federal Tax Authority requires all transactions to adhere to the arm’s length principle regardless of geographic location. This ensures that profit shifting doesn’t occur between mainland entities and free zone entities or between different tax groups within the country’s borders.

What are the penalties for failing to maintain transfer pricing documentation?

Penalties for non-compliance are strictly enforced under Cabinet Decision No. 75 of 2023. A taxable person faces a fine of AED 10,000 for failing to maintain the required records and documentation. If a taxpayer fails to submit the Master File or Local File to the Federal Tax Authority upon request within 30 days, the penalty increases to AED 50,000. These administrative sanctions emphasize the necessity of maintaining a robust governance framework to mitigate fiscal risks.

How does the UAE define “Control” for related party transactions?

The UAE Corporate Tax Law defines “Control” as the ability of a person to influence the conduct of another person through various legal or financial mechanisms. This specifically includes holding 50% or more of the voting rights, owning 50% or more of the share capital, or possessing the power to determine the composition of the board of directors. Such a definition ensures that any entity with significant decision-making authority is subject to the rigorous transfer pricing in the UAE regulations.

Can an SME be exempt from transfer pricing documentation requirements?

Small and Medium Enterprises (SMEs) are exempt from maintaining a Master File and Local File if they don’t meet the specific thresholds set by Ministerial Decision No. 97 of 2023. Currently, documentation is mandatory only if the entity’s revenue in the relevant tax period exceeds AED 200 million or if they’re part of a Multinational Enterprise Group with a total consolidated revenue of AED 3.15 billion. However, all taxable persons must still comply with the arm’s length principle for every transaction regardless of their size.

What is the “Small Business Relief” and how does it affect transfer pricing?

Small Business Relief, established under Ministerial Decision No. 73 of 2023, allows eligible taxable persons with revenue below AED 3 million to be treated as having no taxable income for a given period. While this relief simplifies compliance, it doesn’t entirely negate transfer pricing obligations. Entities must still ensure their related party transactions are conducted at arm’s length to prevent artificial erosion of the tax base, especially if they plan to transition out of the relief in future periods.

How often should a benchmarking study be updated for UAE compliance?

A benchmarking study should generally undergo a full refresh every 3 years to ensure the comparable data remains relevant to current market conditions. While the qualitative search for comparable companies is valid for this triennial period, the financial data of those companies must be updated annually to reflect the most recent economic realities. This meticulous approach ensures that the arm’s length range remains accurate and defensible during a potential Federal Tax Authority audit or review.

What is the deadline for submitting the Transfer Pricing Disclosure Form?

Taxable persons must submit the Transfer Pricing Disclosure Form alongside their Corporate Tax return within 9 months from the end of the relevant tax period. For a business with a financial year ending on 31 December 2024, the submission deadline would be 30 September 2025. This timeline is critical for maintaining your firm’s standing with the regulatory authorities and avoiding the significant administrative penalties associated with late filings or incomplete disclosures.

Do free zone entities have different transfer pricing obligations?

Free zone entities don’t have different transfer pricing obligations and must adhere to the same arm’s length standards as mainland businesses. Maintaining compliance is particularly vital for a Qualifying Free Zone Person to benefit from the 0% preferential tax rate on qualifying income. If an entity fails to conduct transactions with related parties at arm’s length, it risks losing its qualifying status and being subject to the standard 9% corporate tax rate on all income.

Article by

Joseph Mathew

Joseph is a finance and audit professional currently serving as an Audit Manager at Bin Hamad and Mathew Joseph and Associates Chartered Accountants Est., a role he has held since 2022. With a strong background in accounting, compliance, and financial analysis, he brings a detail-oriented and analytical approach to auditing engagements across a range of industries.

In his position at BHMJ Associates, Joseph is responsible for leading audit assignments, overseeing audit teams, and ensuring that financial statements comply with applicable standards and regulatory requirements. He works closely with clients to assess internal controls, identify risks, and provide practical recommendations that enhance financial transparency and operational efficiency.

Known for his professionalism and commitment to accuracy, Joseph has developed a reputation for delivering high-quality audit outcomes within tight deadlines. His ability to interpret complex financial data and communicate insights clearly makes him a valuable advisor to both clients and colleagues.

Joseph continues to build his expertise in auditing and financial management, staying updated with evolving industry standards and best practices, while contributing to the growth and reputation of his firm.

Disclaimer

The content shared and published by Bin Hamad and Mathew Joseph and Associates Chartered Accountants Est. is intended solely for general informational and educational purposes. While every effort is made to ensure the accuracy, completeness, and timeliness of the information provided, the firm makes no guarantees or warranties, express or implied, regarding its reliability or suitability for any particular purpose.

All posts, articles, insights, and commentary do not constitute professional advice, including but not limited to accounting, auditing, tax, legal, or financial advice. Readers are advised to seek appropriate professional consultation before making any decisions based on the information provided.

Bin Hamad and Mathew Joseph and Associates Chartered Accountants Est. shall not be held liable for any direct, indirect, incidental, or consequential loss or damage arising from the use of, or reliance on, the content shared through its platforms.

Any views or opinions expressed in posts are those of the respective authors and do not necessarily reflect the official policy or position of the firm.

By accessing and using this content, you acknowledge and agree to the terms of this disclaimer.